After years of chasing Xero, MYOB is bringing new ideas to market that represent a radical shift in the capabilities of accounting software.

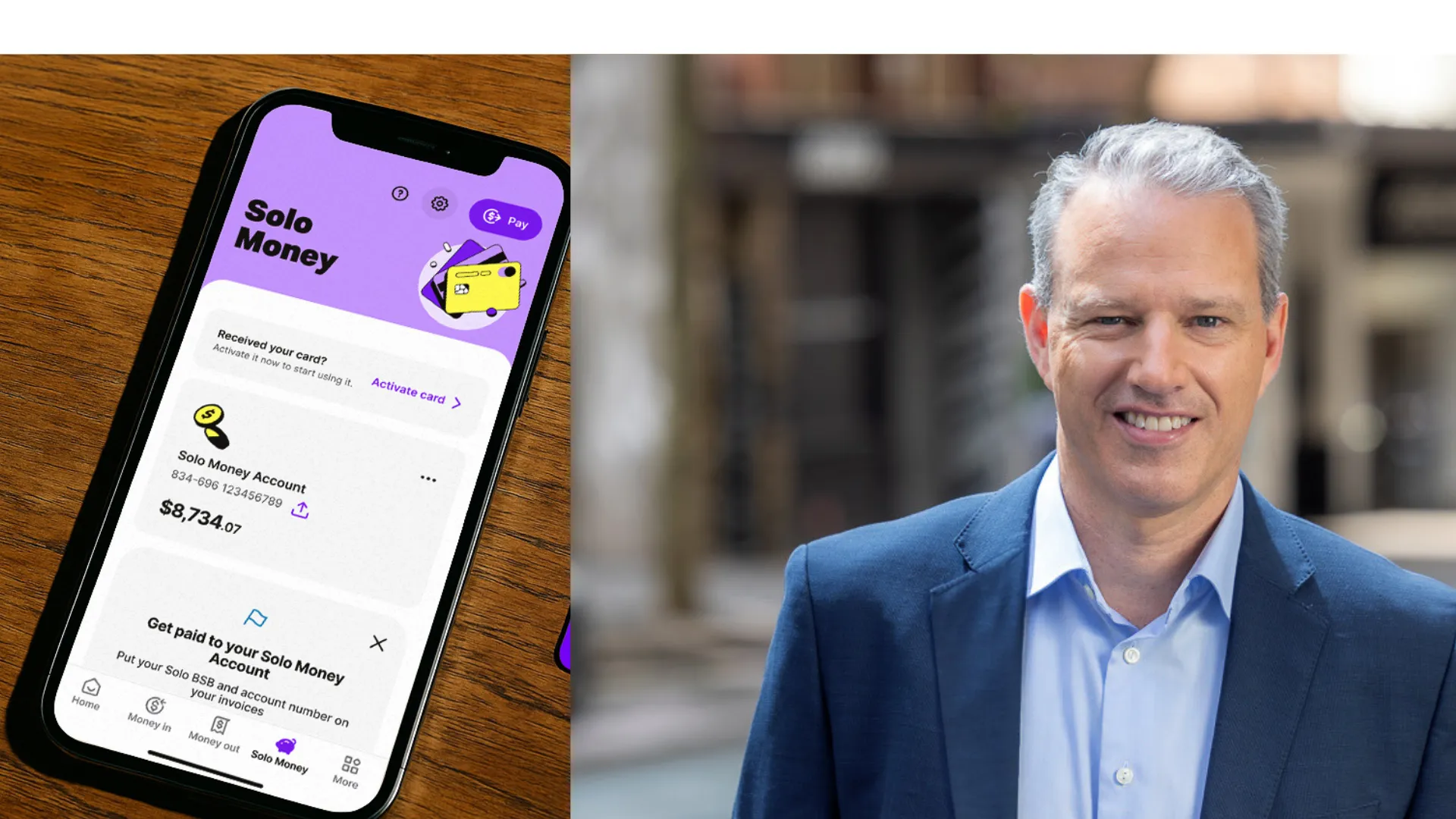

I sat down with MYOB CEO Paul Robson to understand the launch of Solo Money, a transactional bank account embedded directly into MYOB’s new mobile-first product for sole traders.

This matters, because the target market is massive – and largely underserved. “There are 1.6 million sole traders in Australia,” Robson says. “And 74 percent of them don’t use a dedicated business bank account. They’re running their life and business from the same account, with no clear visibility.”

Solo offers a fully mobile, real-time view of cash flow – integrated with a transactional account powered by Great Southern Bank. No ABA files, no switching between apps. Just one interface showing “money in, money out”.

“We’ve built the workflows between banking and accounting so they work together in near real-time,” Robson explains. “You open Solo, see your cash position, upcoming invoices, tax obligations – and you can act on them, right there.”

So what do you call an app that does accounting and banking? Apparently, it’s no longer an accounting app.

“It’s not accounting software,” Robson tells Scale100. “The words we use are ‘admin app’. It’s about helping sole traders manage all the admin of their business in one place – invoices, receipts, payments, and now, the bank account too.”

MYOB’s decision to avoid the “accounting software” label is more than semantics. It reflects a broader shift toward simplicity and accessibility, especially for mobile-native, multilingual business owners who’ve never used desktop accounting systems.

Read on to hear Paul Robson on how Solo was built, what comes next, and why MYOB sees real-time admin as the future of small business tech.

This interview has been edited for clarity and length.

Scale100: Why is MYOB going into this space?

Robson: We're going into this space because we see a tremendous opportunity to aid the productivity of sole traders. There are 1.6 million sole traders in Australia. We know that today, 74 percent of those do not have a dedicated business transaction account. They are running their business and their personal lives from their same bank account.

That isn't necessarily that big a problem for what you call “money in”, when you invoice someone. Where we see a lot of pain for sole traders is the “money out” – was the tap that I just did at the coffee shop a work coffee? Was that stationery? What was that expense? Am I accurately counting the expenses that exist in my business?

The amount of administrative workload that is created for them at the end of each quarter, trying to go back and retrospectively separate business banking from personal banking in a single bank account, is really difficult.

We also know that only 34 percent of sole traders use accounting software today. They actually use their bank account as a proxy, but there's no insight around upcoming invoices that are going to be paid, upcoming expenses, BAS statement, or GST or taxation requirements.

And so by putting those two things together in a single UI (user interface) – so that when you take an action it impacts journal entry workflow and banking workflow – means that if you're a sole trader, a plumber or someone in a market stall on a weekend, you open the app and you see real-time cash, real-time insight and the health of your business, right there and then.

Scale100: That’s a huge change. So they don’t need to go to the bank to manage their bank account? It’s all in the accounting software?

Robson: Yes, it's in Solo, the app. We think of the app as an all-in-one admin device, not accounting software or banking software. Solo is providing them with visibility of both.

Scale100: That's interesting that you don't classify Solo as an accounting app.

Robson: The words that we use is it’s an admin app. We see it as a way for you to just deal with all the admin for your business. We've changed the terminology.

The demographic of somebody who starts a business in Australia as a sole trader today is changing; they're younger. In many cases, English isn't their first language. They're newly arrived Australians. They've come from markets where there is no desktop computing. They've come from economies where everything is mobile. Businesses are run on WhatsApp.

Think about newly arrived Australians from places like China or India or Southeast Asia. It's a different way of working than the traditional desktop environment. If you think about it through that lens, you need an admin assistant in your pocket that is fully mobile. But the history of accounting software (in Australia) has always been desktop.

So we put that into a mobile device and add tap-to-pay and other functionality. Not only are we changing the terminology from an accounting app to an admin app, we've changed the terminology around invoicing and receipt management.

If you open Solo you see “money in” and “money out”. It becomes a very clear way for users to understand basic accounting workflows. Money leaves your bank account – that's an expense. Money comes in – that's typically revenue.

And then it has to go through a journal entry into a ledger and into a set of financial statements. That's the piece that a lot of sole traders struggle with. They're great at setting up and running businesses. They're not always great at the admin and that's the bit we're breaking down.

Scale100: What does an admin app include then? So you've got a bank account in there, you have accounting, what else?

Robson: Start at the macro level. Businesses start, survive and succeed based on cash management. We are solving your ability as a sole trader to have a very clear, near real-time view of your cash position. Money that's going in, money that's coming out. Inside that are detailed, deep accounting workflows. Inside that is access to technology like tap-to-pay and other embedded financial solutions. Inside that is access to a transactional bank account that you can connect.

Even though we're launching Solo Money and would like as many of our customers to take it up as possible, we are also allowing you to connect an existing bank account through traditional open banking. The difference is that the MYOB branded account shows transactions in near real-time.

Scale100: Can you pay for other bills within the app? With a BSB and account number?

Robson: Yes, you can pay with your transaction bank account by transferring money inside Solo.

Scale100: How did you get Great Southern Bank to agree to that? That means they have no access to the customer.

Robson: First of all, this has been a long journey to build out the bank account. It’s taken two years. It's a partnership between us and Great Southern Bank. The bank account is Great Southern Bank, and it's branded Solo Money on an MYOB app.

We effectively surface and show the bank account details as part of the app, and we spent two years building the interfaced workflows between accounting and banking transactions so that they sit and work together in near real-time. When you open the bank account inside Solo, you have your balance, you can transfer, you can pay, you can receive money. It’s a bank account in the Solo app.

Scale100: Doesn't that mean that the Great Southern can't flog their home loans and bank loans and all their other products? Do you think banks will lie down and just become wholesale infrastructure providers?

Robson: We're talking right now about transactional bank accounts. If the sole trader then decides that they want to start looking at financing solutions, they can do that through Great Southern or other banks and the like.

Scale100: I understand. I'm just curious that a bank would be happy to give up the whole customer relationship. Because if a sole trader on MYOB Solo wants a business loan, there’s no form to open up a loan with Great Southern within the app, or even a link to a landing page, right?

Robson: We're launching the transaction bank account now. We're working with Great Southern Bank on other offerings for the future. But I actually wouldn't see this as a ceding of the customer relationship. It truly is a partnership between the two of us providing an opportunity for that sole trader to have a relationship with the admin app. The app drives that interface.

You talked about payment companies before. Payment companies think that they have the most amazing perspective of the health of the customer because they see transaction history.

I would argue that an accounting software provider actually has a far more detailed view of the financial health of the business. Because we see the general ledger, we see the balance sheet, and there's far more that happens to a business than just payments.

You see payroll. You see the number of employees. You see employees onboarded, etcetera. And so I think the power of the accounting side of that equation is very strong around understanding the fiscal health of the business, and that represents future opportunities for us to work with partners on.

Scale100: I see. So, theoretically, you could offer information to Great Southern Bank about the fiscal health of potential customers who may want to take out a loan, which would reduce their cost of lending?

Robson: I would say it in a different way. Theoretically, if the customer asked us, we could allow them to get access to other financial services. The customer makes that call. The customer says, I want to do something to help me. That information that we could surface to them is very powerful for them to use.

So again, a perfect example is the plumber. If a plumber decides that they want to borrow some money to buy some tools. They call a lender. The lender says, Can you give me some financial statements, financial history, cashflow? The plumber says, how do I do that? Now with Solo, that's all surfaced in a daily dashboard.

Scale100: How does the banking integration work within the accounting workflow?

Robson: The best example of this is a plumber. A plumber comes to your house, fixes your leaking tap. In the past, they would have gone home, generated an invoice, sent you that invoice, you would have paid it overnight, maybe it took two days for the money to clear. At some point in the future, they would have had to either do a manual reconciliation or hope that the system kind of connected those two things together.

Today, the plumber finishes the leaking tap, and tap-to-pay means you can pay him immediately. MYOB Money on Solo does two things immediately. It starts the journal entry for the accounting workflow, and it also shows the money in your bank account. We call it “near real-time”, because it's not exactly to the second, but a near real-time view of cash flow.

So it addresses the issue where a lot of businesses will transact all day, but need to wait for the clearing activities to happen through the traditional way open banking works today. And that's the power of connecting the two together. That's number one.

Number two is that through the Solo app you'll be able to see not only your accounting workflow transactions – invoices that are outstanding, receipts that need to be reconciled – but you'll also see your bank balance. Again in near real-time, and this is where we use data science to serve up insights.

So we can show you a dashboard that talks to real-time cash flow. You can interrogate your own business to say, “Do I have enough cash right now to pay my next BAS statement? Do I have enough cash to make this investment? Am I chasing invoices?” It's effectively all in that one app.

Scale100: Intuit did this about seven years ago, and it's also in the UK as well. It’s great that this concept is now in Australia. Do you see this as an inevitable trajectory for accounting software, or admin apps, to add banking within the app?

Robson: Every market is very different. It's very hard to compare market to market because accounting and banking are such regulated environments.

I would say that if your mission is to solve for removing administrative burden to sole traders and small businesses, the more that we can do to provide them visibility of the health of their business, to make real time decisions based on their current fiscal position, is incredibly valuable to the sole trader and to the small business.

So that's what everyone has come at it from, I would imagine. We believe that we will drive loyalty and engagement with our customers based on being able to provide them a greater level of support, visibility, insight and data around their business.

Customers that have started using MYOB Solo before the launch of MYOB Money are telling us they're saving 17 hours a month on average. It is near enough to three working days. That’s the Sunday afternoon invoice run, or the Friday night reconciliations.

Scale100: So, by that logic, it would make sense then to add bank counts to MYOB Business?

Robson: Right now we're focused on Solo.

Scale100: Because it makes sense. Everything you said about all those time savings and near real-time banking, that is true for every single business owner. I don't care what they're running.

Robson: Right now we are focused on Solo. We continue to press on driving features, functions and releases that reduce administrative burden for all of our customers across all of our platforms.

Scale100: I'm very glad to hear. It is great to see MYOB making bold moves like this. I have some specific questions around Hnry and whether you are thinking about adding vertical services such as bookkeeping, which Intuit has also done.

Robson: We don't talk about our competitors.

Scale100: I'm just interested whether you will add bookkeeping or accounting services into the app, as others have done.

Robson: Bookkeepers and accountants are a really critical part of the ecosystem. In Australia, you are required to have an accountant sign off on statutory financial statements. Bookkeepers have a long, long future, and we can have a whole other conversation about AI and disruption, but accountants and bookkeepers are not going anywhere fast.

What I would say is that bookkeepers are equally as excited as we are about many of the features inside Solo because it reduces a lot of the administrative burden that comes to a bookkeeper.

Bookkeepers want to get into more conversations where they assist their customers in making the right decisions around how to run and operate their business. What bookkeepers don't like is when you turn up with a shoebox full of receipts and say, Can you just work this out for me?

One of the biggest (groups of advocates for) Solo are bookkeepers. It breaks down the start of the process. The better the start of the process, the more effective that bookkeeper becomes.

So if you go and interview bookkeepers they'll say, the best businesses that we work with are those that actually know what they're doing, do some of the accounting work themselves and work with us in a more sophisticated environment. It’s not the customers that say, “I'm hands off. Here's all the data. Please help me out.” And so I actually see the two things merging closer together. What we are providing is feature and function that supports the bookkeeping function, it doesn't replace it.

Image credit: MYOB